How WestEnd Actively Manages Portfolio Risk

Many investors and financial advisors define “risk” by how a portfolio looks. If there are fewer than 50 stocks or if one sector or industry is meaningfully overweight, the immediate conclusion is often that the portfolio isn’t sufficiently diversified—and is therefore too risky.

We think differently.

In our view, risk in an equity portfolio comes from owning businesses with deteriorating fundamentals, slowing earnings, weakening demand, or limited upside relative to the price being paid for shares. When an investment portfolio mimics an index or broadly diversifies for the sake of managing risk, it sometimes means owning dozens or even hundreds of companies with lackluster or negative earnings growth. We don’t see this as sound risk management.

By contrast, our approach to managing risk means owning companies with strong earnings power, durable competitive positions, and proven management teams. Put differently, we want our exposure concentrated where the earnings power is most compelling, not spread indiscriminately across the market.

Consider a few examples from the Core portfolio (as of June 30, 2026). Since early March, consensus earnings estimates have moved meaningfully higher for companies like Quanta Services, Eli Lilly, and Howmet Aerospace. Rising earnings estimates are not the whole story, but they are one of the clearest external signals that business momentum is moving in the right direction.

We spend a great deal of time stress-testing the portfolio, thinking through bad-day scenarios, and evaluating how position sizes would behave in more difficult market environments. We do not assume that because a company is high quality today, it will always deserve the same weight tomorrow. If one of our companies stops beating, merely meets expectations, or starts to show signs of fundamental trouble, we have a long history of acting quickly. In that sense, risk management is embedded in every position we own.

Looking out at the marketplace, we would argue that many managers are structurally prevented from making the type of active decisions we make at WestEnd. Being benchmarked to the S&P 500 index, for example, usually requires having exposure to every sector in the S&P 500, even if the outlook is negative. A case-in-point is 2022, where many managers found themselves over-allocated to technology stocks, while also being stuck holding stocks with high P/E ratios and the prospect of weaker earnings. To demonstrate this point, just take a look at the 2022 performance of some of the top holdings in the S&P 500:

Apple, Inc: -31.28%

Microsoft Corp: -28.43%

Amazon.com Inc: -49.64%

Alphabet Inc A: -38.53%

Meta: -63.15%

Tesla: -72.69%

We knew at the time that these were all fantastic companies.

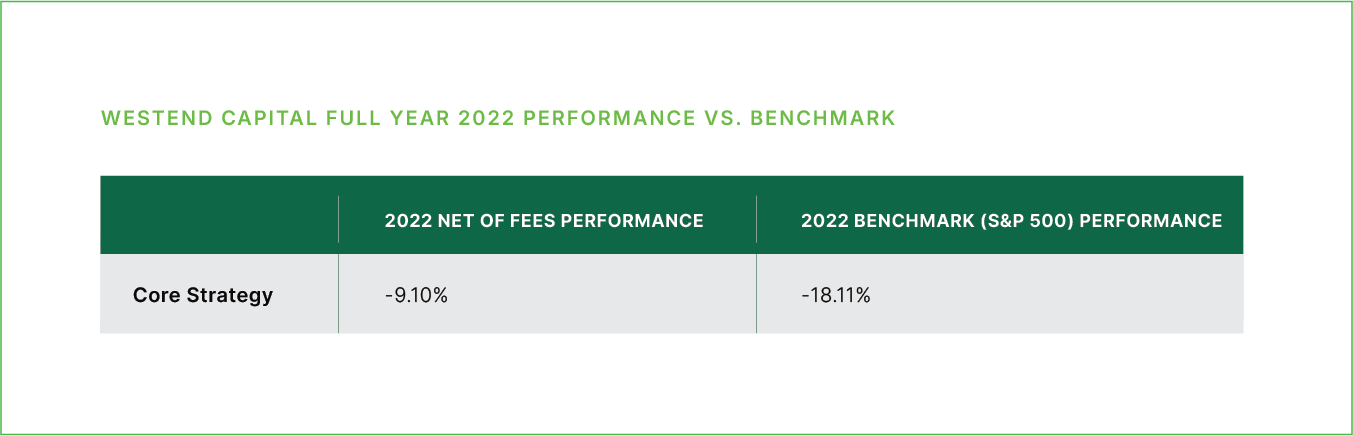

Our approach to risk management meant we avoided these companies in 2022, and we instead tilted the portfolio towards value stocks because of the rapidly shifting environment. Our positioning substantially cushioned the downside for the year, with our Core Strategy falling -9.10% in 2022 compared to the S&P 500’s -18.11% loss and the Nasdaq’s staggering -32.5% selloff.

How We View Effective Risk Management

*Performance values as of December 31, 2022

Please note that these performance figures represent a weighted average of return for each strategy, based on a sampling of actual accounts. The accounts used to measure weighted average performance were generally portfolios that were invested for the entire quarter and were not subject to extraneous factors like scheduled withdrawals, account restrictions, and other factors. The weighted average was based on 102 Core portfolios. Actual performance results may differ from composite returns, depending on the size of the account, investment guidelines and/or restrictions, inception date and other factors. Please see the index disclaimers for the S&P 500 at the end of this review. Past performance is not indicative of future results.

If a key feature of managing risk is how a manager performs during a bear market, we think our track record demonstrates our capabilities. More broadly, we believe risk is best managed not by owning more stocks for the sake of appearance, but by owning the right businesses, monitoring them closely, and acting decisively when conditions change.

As we cross the midpoint of the year, we remain laser focused on finding companies with resilient earnings power and strong long-term prospects. We believe that focus, combined with active oversight and a willingness to adapt when conditions change, is central to how we manage portfolio risk. If you have any questions about the portfolio or our approach to risk management, please feel free to reach out to any member of the WestEnd team.

Notes and Disclaimers

This newsletter has been prepared solely for the client to whom it was directed and may not be sent to any other party. Further, it contains highly confidential and proprietary information and trade secrets that are of independent, economic value to us. Any disclosure of this information could cause us competitive harm. By accepting this newsletter, you agree to keep strictly confidential all of its contents and may not reproduce, distribute, share or publish in any manner without our prior written consent. This letter is not, and is not intended to be, an advertisement within the meaning of Advisers Act Rule 206(4)-1.

Further, a substantial part of this newsletter contains forward-looking statements within the meaning of the federal securities laws, including in particular statements appearing on page 3. Forward-looking statements are those that predict or describe future events or trends and that do not relate solely to historical matters. For example, forward-looking statements may predict future economic performance, describe plans and objectives of management for future operations and make projections of revenue, investment returns or other financial items. A prospective investor can generally identify forward-looking statements as statements containing the words “will,” “believe,” “expect,” “anticipate,” “intend,” “contemplate,” “estimate,” “assume” or other similar expressions. Such forward-looking statements are inherently uncertain, because the matters they describe are subject to known (and unknown) risks, uncertainties and other unpredictable factors that are beyond our control. Actual results could and likely will differ, sometimes materially, from those projected or anticipated. We are not undertaking any obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise. You should not take any statements regarding past trends as a representation those trends or activities will continue in the future. Accordingly, you should not put undue reliance on these statements.

In preparing this newsletter, we have relied upon information provided by the custodian(s) and other third-party sources we believe to be reliable and accurate.

Past performance does not guarantee future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable. Changes in investment strategies, contributions or withdrawals, and economic and market conditions will materially alter the performance of your account. All investing involves risk of loss including the possible loss of all amounts invested.

Index Disclaimers

The benchmarks referenced are included to reflect the general trend of the markets during the periods indicated and are not intended to imply that the underlying returns were comparable to the market indices either in composition or element of risk. There are significant differences between client accounts and the indices herein including, but not limited to, risk profile, liquidity, volatility, and asset composition.

The S&P 500 Index is a capitalization-weighted index comprised of 500 stocks chosen for market size, liquidity and broad industry group representation within the U.S. economy. Index returns represent gross returns, and are provided to represent the investment environment during the time periods shown and are not covered by the report of the independent verifiers.