Q1 2026 Strategy Update and Market Review

Quarterly Reports – Now Posted

Check your WestEnd Black Diamond Portal for the latest performance report through the most recent quarter’s end.

If you need help logging in, contact us directly or visit this page for instructions: Client Login Information

At one point earlier in the new year, we thought the sharp selloff in software stocks would be the biggest story to cover in Q1. There was also the Supreme Court’s decision on tariffs and the criminal referral of a sitting Federal Reserve Chairman.

The news cycle moves fast.

As we write, a two-week cease-fire has taken hold between the U.S. and Iran, pausing a conflict that sent oil prices and market volatility sharply higher in recent weeks. Shipping disruptions in the Strait of Hormuz and the U.S. naval blockade of Iranian ports continue to cloud the near-term outlook. But as we’ve been seeing in recent trading sessions, the market may have already moved past this crisis. During World War II, the stock market bottomed just five months into the conflict even as the war went on for nearly five more years. Headline risk around Iran is likely to persist for some time, but we think its pricing power may continue to diminish.

WestEnd’s Core Portfolio proved resilient during the quarter’s downside volatility, outperforming the S&P 500 by over 9%.

*Performance values as of March 31, 2026

Please note that these performance figures represent a weighted average of return for each strategy, based on a sampling of actual accounts. The accounts used to measure weighted average performance were generally portfolios that were invested for the entire quarter and were not subject to extraneous factors like scheduled withdrawals, account restrictions, and other factors. The weighted average was based on 131 Core portfolios. Actual performance results may differ from composite returns, depending on the size of the account, investment guidelines and/or restrictions, inception date and other factors. Please see the index disclaimers for the S&P 500 at the end of this review. Past performance is not indicative of future results.

The Core Strategy’s bias toward industrial, infrastructure, and energy-related businesses was well-suited for an economic landscape increasingly focused on energy independence, supply-chain security, domestic production, defense readiness, and infrastructure resilience. The war has certainly reinforced these themes, but even without the fighting, we also believe the artificial intelligence story is increasingly an energy and industrial story. It’s all about data centers, power generation, grid investment, and physical inputs.

Consider the performance of our top five holdings (by % weight as of March 31, 2026) compared to the S&P 500 in the first quarter:

Century Aluminum (CENX): +88%

Cameco Corp (CCJ): +23%

Kodiak Gas (KGS): +61%

Freeport-McMoran (FCX): +13.2%

Quanta Services: +26%

S&P 500: -4.3%

Another driver of Core’s outperformance in the quarter was our decision to raise cash in the portfolio in March. We strategically trimmed exposure in some of our more expensive growth and higher-PE names, including Apple, Boeing, GE Aerospace, Eli Lilly, Howmet, and Viking. We also fully exited Circle with capital gains and sold Rheinmetall, which was disappointingly mostly flat. We brought cash to more than 10% in the Core portfolio, which helped cushion downside during the quarter’s sharpest pullback while giving us flexibility as we head into Q1 earnings season.

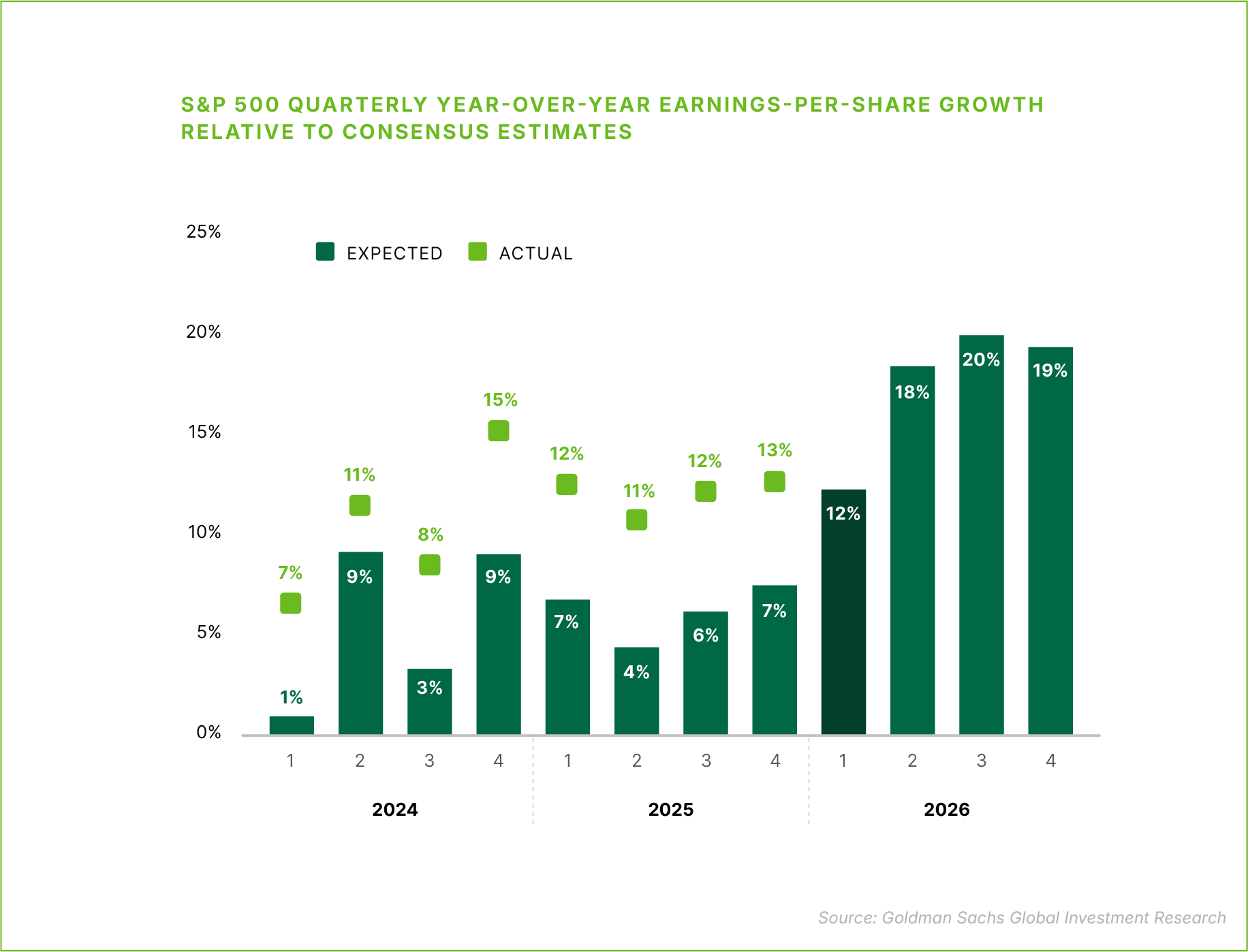

On that note, despite the geopolitical shock and ongoing uncertainty in Iran, earnings expectations for 2026 continued to move higher during the quarter, suggesting little to no impact on the profit outlook. We think this underscores not only the remarkable resilience of the U.S. economy, but also the idea that we’re still firmly in the growth phase of the cycle.

Total S&P 500 earnings for the first quarter of 2026 are currently expected to rise ~12% from a year earlier on ~9% higher revenues, following 13% earnings growth on 9% revenue growth in Q4 2025. Technology remains the largest growth engine, with the sector expected to deliver 27% earnings growth in the current quarter. But even excluding Technology, S&P 500 earnings are still projected to grow ~6%, which suggests the profit backdrop is becoming less narrowly concentrated than it was over the last two years.

Nevertheless, we expect risk and recession headlines to remain pervasive for weeks if not months, as the conflict runs its course. There are longer-term scenarios where severe energy disruption could change our outlook. But at this stage, we are not convinced that geopolitical conditions will adversely impact demand across our portfolio companies.

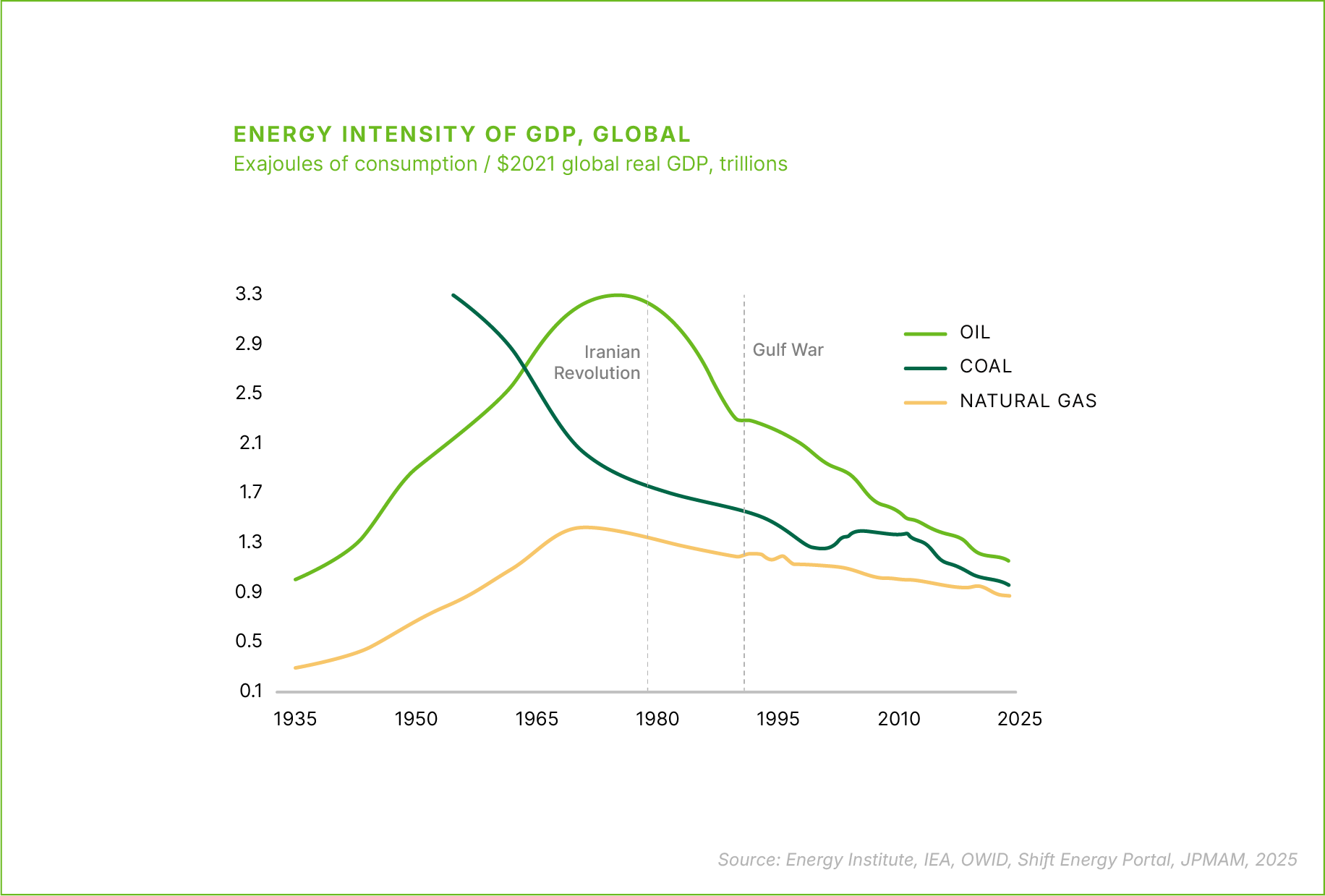

Global economic growth—and especially U.S. economic growth—is far less dependent on oil than it was decades ago. Oil use relative to GDP has fallen sharply from its 1970s peak and now stands at roughly half the level seen during the Gulf War in 1990 (see chart below). As a result, oil price spikes generally have a smaller effect on growth and profits than they once did, and we think markets are already starting to reflect this reality.

The first quarter also showed us how quickly sentiment can shift as investors reassess the pace and impact of technological change. A update in Anthropic’s Claude product, which demonstrated AI’s ability to generate and execute complex workflows, contributed to a selloff in select software names and reignited debate around the durability of certain business models.

Investors are more seriously considering the possibility that AI could pressure parts of the SaaS model rather than simply enhance it. Our skepticism towards many software names has been building for some time, particularly where valuations were high and long-term differentiation looked more vulnerable than the market appreciated. Our caution last year proved helpful in Q1 2026. Being out of names like Snowflake, Palantir, UiPath, and ServiceNow meant avoiding sharp drawdowns:

Snowflake: we sold in mid-December at roughly $214; recently trading around $134

Palantir: we sold in November at roughly $188; recently trading around $135

UiPath: sold at roughly $14; recently trading around $9

ServiceNow is down nearly -50% over the past year

Expectations ran too far ahead of these and other companies, with even well-liked software names getting repriced hard. More broadly, the selloff reinforced a view we have held for years: not every AI beneficiary will be a winner, and in some corners of the market, AI may prove more disruptive than additive.

Active Management + Hands-On Research

Periods like this reinforce why active management has to extend beyond financial analysis and macro forecasting. There are portfolio-level insights you simply cannot get from a desk chair, even with all the advances in technology and data now available.

That is why WestEnd continued to do on-the-ground research throughout the quarter.

In Texas, George Bolton and Ali met with Kodiak Gas, and George Elliman joined them for a meeting with Kinetik as a potential future addition to Core portfolios (the company remains on our watch list). The following week, George Bolton and Ali were in New York for Quanta Services’ 2026 Investor Day, where they had the opportunity to hear management’s long-term outlook directly, meet with senior executives, and speak with other analysts and customers. This kind of firsthand access helps us test assumptions, refine conviction, and better understand how company-level fundamentals are evolving.

Ali also attended two of the year’s major technology conferences during the quarter: CES 2026, the annual Consumer Technology Association event held in Las Vegas in January, and NVIDIA GTC 2026, NVIDIA’s annual developer and AI conference held in San Jose in March.

CES is a broad showcase for emerging technologies and industry direction, while GTC is more focused on the hardware, software, and applications shaping AI, robotics, inference, and next-generation computing. Ali’s in-person research and conversations with industry insiders provided useful perspective on several portfolio holdings, including Caterpillar, Google, and Rockwell, while also sharpening WestEnd’s broader view of where demand, competition, and capital spending trends may be headed.

Firsthand research is a key part of how we navigate markets like these. Volatility and uncertainty are part of investing, but they also create opportunity for disciplined, active managers willing to do the work. We remain focused on bottom-up research, thoughtful risk management, and identifying the businesses best positioned for the environment ahead.

If you have any questions about this review or your portfolio, please do not hesitate to reach out. We hope you’re enjoying the transition to spring.

Notes and Disclaimers

This newsletter has been prepared solely for the client to whom it was directed and may not be sent to any other party. Further, it contains highly confidential and proprietary information and trade secrets that are of independent, economic value to us. Any disclosure of this information could cause us competitive harm. By accepting this newsletter, you agree to keep strictly confidential all of its contents and may not reproduce, distribute, share or publish in any manner without our prior written consent. This letter is not, and is not intended to be, an advertisement within the meaning of Advisers Act Rule 206(4)-1.

Further, a substantial part of this newsletter contains forward-looking statements within the meaning of the federal securities laws, including in particular statements appearing on page 3. Forward-looking statements are those that predict or describe future events or trends and that do not relate solely to historical matters. For example, forward-looking statements may predict future economic performance, describe plans and objectives of management for future operations and make projections of revenue, investment returns or other financial items. A prospective investor can generally identify forward-looking statements as statements containing the words “will,” “believe,” “expect,” “anticipate,” “intend,” “contemplate,” “estimate,” “assume” or other similar expressions. Such forward-looking statements are inherently uncertain, because the matters they describe are subject to known (and unknown) risks, uncertainties and other unpredictable factors that are beyond our control. Actual results could and likely will differ, sometimes materially, from those projected or anticipated. We are not undertaking any obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise. You should not take any statements regarding past trends as a representation those trends or activities will continue in the future. Accordingly, you should not put undue reliance on these statements.

In preparing this newsletter, we have relied upon information provided by the custodian(s) and other third-party sources we believe to be reliable and accurate.

Past performance does not guarantee future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable. Changes in investment strategies, contributions or withdrawals, and economic and market conditions will materially alter the performance of your account. All investing involves risk of loss including the possible loss of all amounts invested.

Index Disclaimers

The benchmarks referenced are included to reflect the general trend of the markets during the periods indicated and are not intended to imply that the underlying returns were comparable to the market indices either in composition or element of risk. There are significant differences between client accounts and the indices herein including, but not limited to, risk profile, liquidity, volatility, and asset composition.

The S&P 500 Index is a capitalization-weighted index comprised of 500 stocks chosen for market size, liquidity and broad industry group representation within the U.S. economy. Index returns represent gross returns, and are provided to represent the investment environment during the time periods shown and are not covered by the report of the independent verifiers.